- June 15, 2026

- Pathik Shah

Key Points in AML Laws for Estate Agents in Hong Kong

- Estate agents in Hong Kong are subject to AML/CFT requirements when they are involved in a transaction concerning the buying or selling of real estate for a client.

- Core statutory obligations under AMLO focus on customer due diligence (CDD), beneficial ownership identification, ongoing monitoring where applicable, and record-keeping.

- Suspicious transaction reporting obligations arise under DTROP, OSCO, and UNATMO, with reports filed with the JFIU. The Estate Agents Authority (EAA) supervises the sector under Practice Circular No. 23-01(CR).

- While the sector is rated medium-low risk, estate agents should maintain robust controls around complex ownership structures, opaque funding sources, and third-party purchasers.

AMLO: Scope and Applicability for Estate Agents in Hong Kong

Hong Kong’s AML/CFT framework applies to entities operating within the real estate sector, particularly those facilitating transactions involving property buyers and sellers.

Estate agents are designated as Designated Non-Financial Businesses and Professions (DNFBPs) under Section 1 in Part 2 of Schedule 1 to the AMLO. Under Section 5A(4) of the AMLO, estate agents are subject to statutory CDD and record-keeping requirements under Schedule 2 when involved in a transaction concerning the buying or selling of real estate for a client.

The estate agency sector carries a medium-low ML/TF risk rating, though vulnerabilities exist where transactions involve complex ownership structures (such as shell companies) or opaque sources of funds.

The estate agents’ AML guidelines require firms to adopt a risk-based approach, ensuring appropriate controls are applied depending on the risk profile of clients and transactions.

This is especially important where the customer, source of funds, beneficial owner, corporate structure, or transaction arrangement has a cross-border or offshore element.

Estate agents must implement Customer Due Diligence (CDD) when involved in a transaction concerning the buying or selling of real estate for a client. These requirements aim to prevent misuse of the property sector for money laundering and terrorist financing.

When Should Estate Agents Conduct CDD?

Estate agents should conduct CDD before establishing a business relationship with a customer or before carrying out relevant property transaction work, as required under Schedule 2 to AMLO and the EAA Guidelines. CDD should cover the customer, any person purporting to act on behalf of the customer, and beneficial owners where applicable. Enhanced due diligence should be applied where higher ML/TF risks are identified, including PEP involvement, complex ownership structures, unusual source of funds, unusual source of wealth, sanctions exposure, or other red flags.

Core AML/CFT/CPF Laws and Regulations for Estate Agents in Hong Kong

Estate agents should understand the following AML/CFT/CPF legislation relevant to their role.

The key laws and regulations are summarised below.

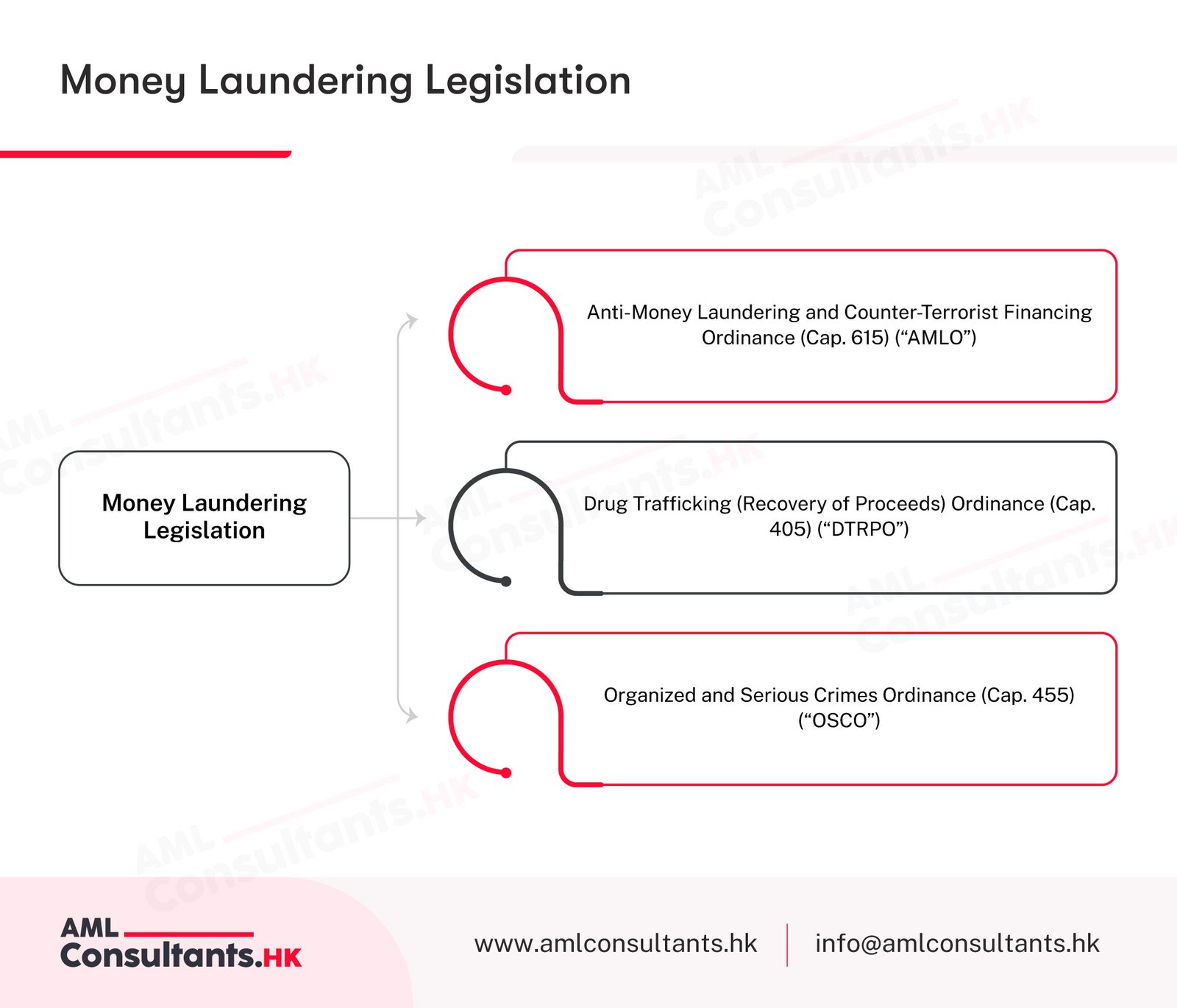

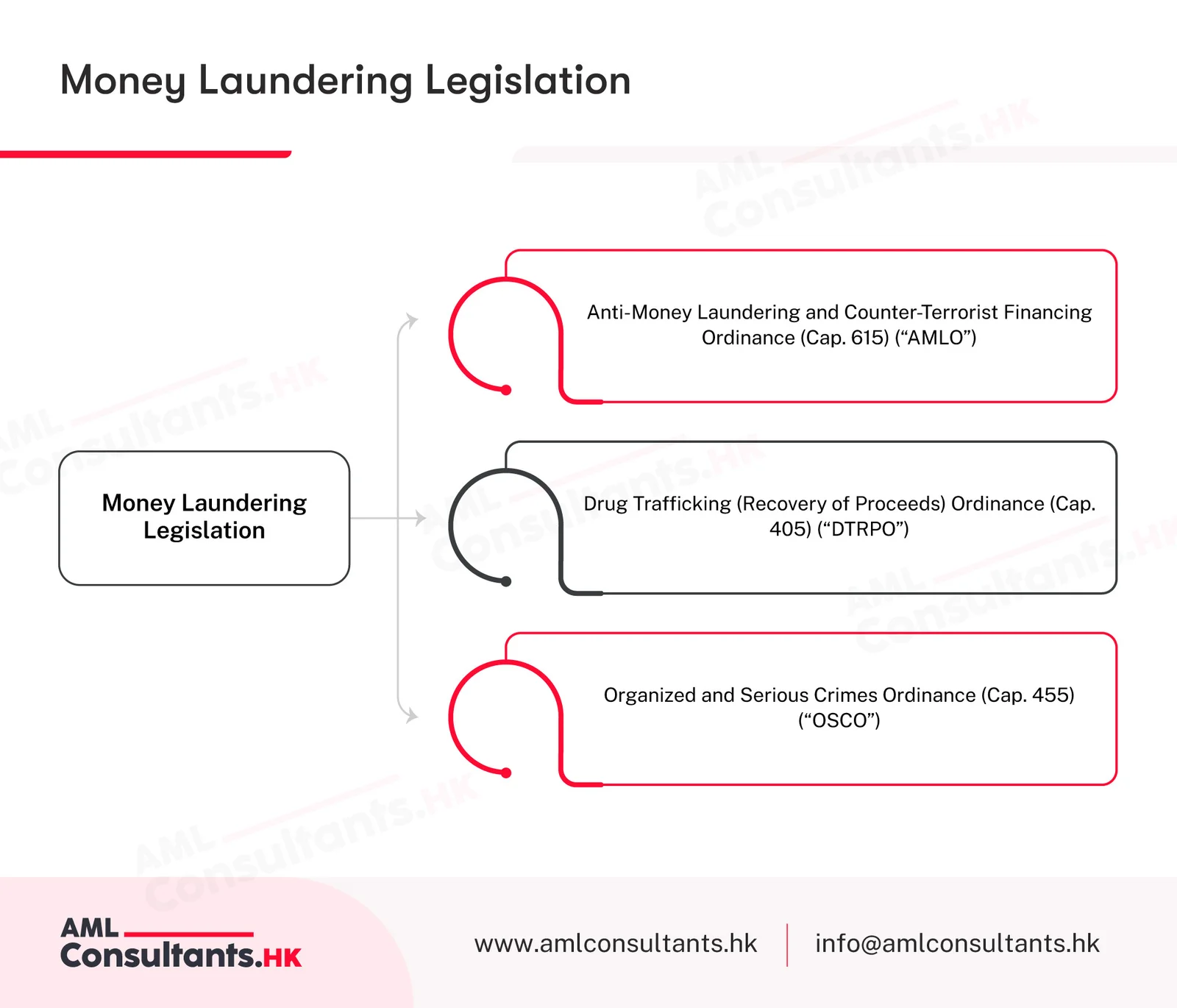

Money Laundering Legislation

The primary AML/CFT legislation applicable to estate agents in Hong Kong is the Anti-Money Laundering and Counter-Terrorist Financing Ordinance (AMLO) (Cap. 615). AMLO imposes statutory CDD and record-keeping obligations on estate agents under Schedule 2 when they are involved in a transaction concerning the buying or selling of real estate for a client.

The Drug Trafficking (Recovery of Proceeds) Ordinance (DTROP) Cap. 405 applies to estate agents in Hong Kong by imposing a mandatory reporting obligation when they know or suspect that property involved in a transaction represents the proceeds of drug trafficking. Estate agents must disclose any such knowledge or suspicion to the JFIU by filing a Suspicious Transaction Report (STR), particularly where there are indicators of unexplained or suspicious sources of funds.

The Organised and Serious Crimes Ordinance (OSCO) Cap. 455 applies to estate agents and other persons by creating offences relating to dealing with proceeds of indictable offences, imposing suspicious transaction reporting obligations where knowledge or suspicion arises, and prohibiting tipping off in relevant circumstances. Under section 25 of OSCO, it is a criminal offence for any person, including estate agents facilitating property transactions, to deal with property knowingly or having reasonable grounds to believe that it represents the proceeds of an indictable offence.

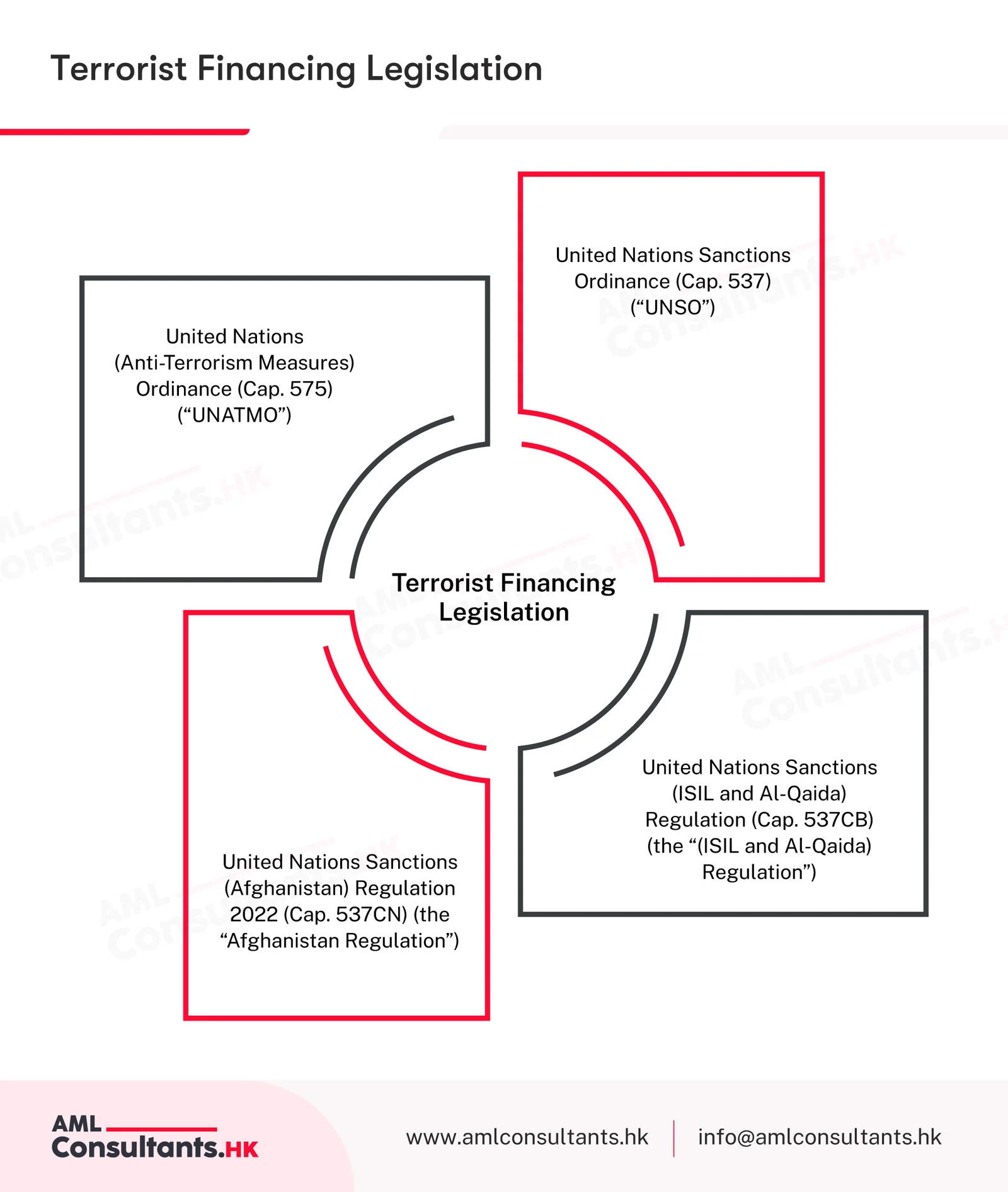

Terrorist Financing Legislation

- The United Nations (Anti-Terrorism Measures) Ordinance (UNATMO) Cap. 575 is the principal legislation criminalising terrorist financing in Hong Kong. It implements UN Security Council Resolution 1373 and creates standalone offences for providing or collecting property with the intention or knowledge that it will be used to commit terrorist acts (section 7), as well as for dealing with terrorist property or making property or financial services available to terrorists or terrorist associates. UNATMO also empowers authorities to freeze and seize terrorist property. Estate agents must not facilitate any property transaction where there are grounds to suspect the property is linked to terrorism.

- United Nations Sanctions Ordinance (UNSO) Cap. 537 implements sanctions imposed by the UNSC in Hong Kong. Under the UNSO, subsidiary regulations such as the ISIL and Al-Qaida Regulation and the Afghanistan Regulation give effect to targeted financial sanctions, asset freezes, and travel bans directed at designated terrorists and terrorist entities. Estate agents must ensure compliance with these sanctions as a statutory obligation, including screening parties to property transactions against published sanctions lists.

- The United Nations Sanctions (ISIL and Al-Qaida) Regulation (Cap. 537CB) (the “(ISIL and Al-Qaida) Regulation”) prohibits the supply or transfer of arms, military-related assistance, and funds or economic assets to ISIL and Al-Qaida designated persons and entities. Estate agents must screen transaction parties against the published sanctions list.

- The United Nations Sanctions (Afghanistan) Regulation 2022 (Cap. 537CN) (the “Afghanistan Regulation”) implements UNSC sanctions on Afghanistan by prohibiting arms supply, imposing targeted financial sanctions, and restricting economic assets to designated persons and entities. Estate agents must ensure that no deposits or transaction proceeds under their control are made available to designated persons.

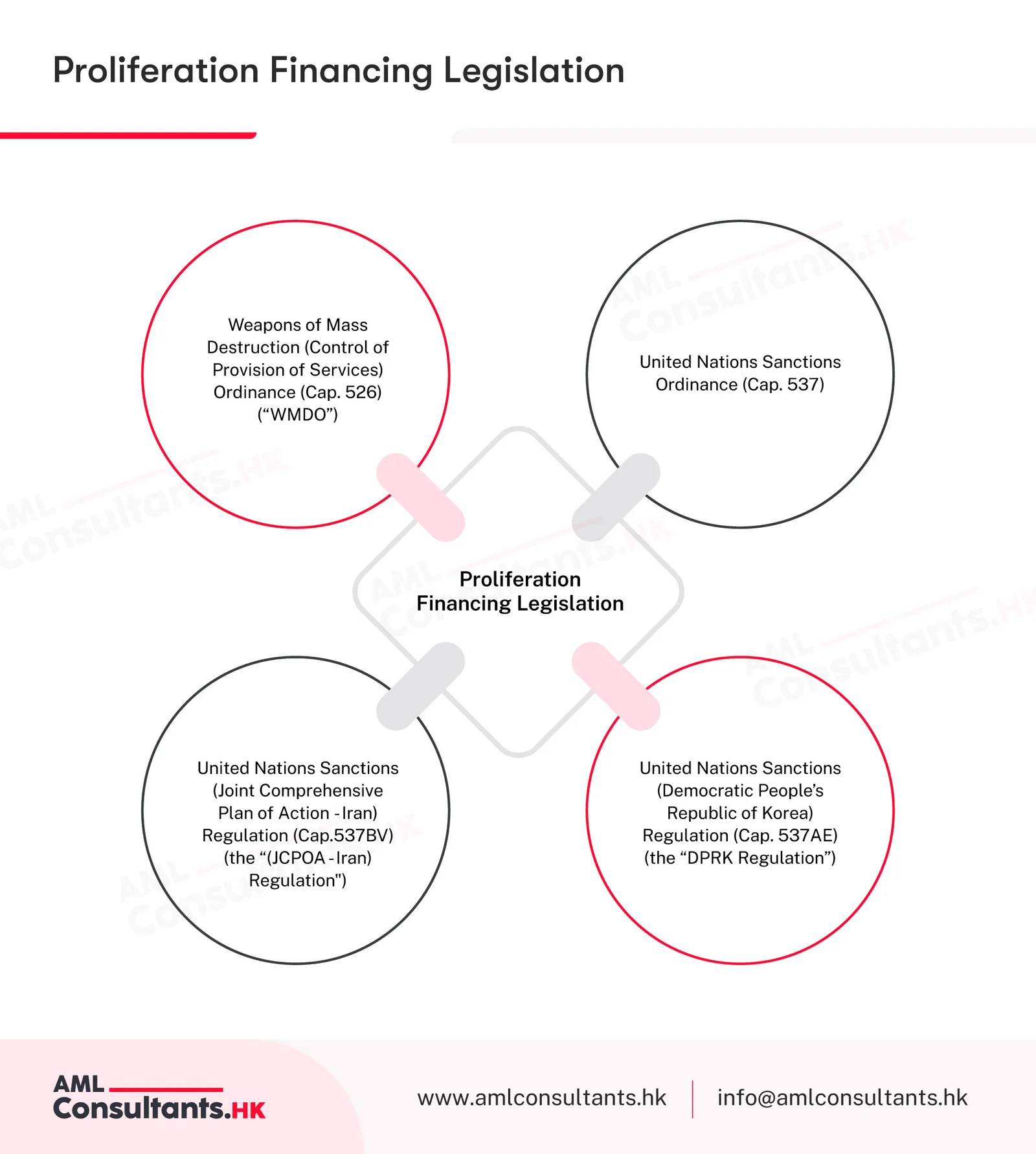

Proliferation Financing Legislation

- The Weapons of Mass Destruction (Control of Provision of Services) Ordinance (WMDO) Cap. 526 prohibits any person from providing services that will or may assist the development, production, acquisition, or stockpiling of weapons of mass destruction. “Services” is broadly defined to include financing, sourcing of materials, training, technological information, and consulting. While WMDO risks may be less common in ordinary estate agency work, estate agents should ensure that their services are not used in a way that may assist prohibited proliferation-related activity.

- United Nations Sanctions Ordinance (UNSO) Cap. 537 is the parent ordinance empowering the Chief Executive to make regulations implementing UNSC sanctions in Hong Kong. In the proliferation financing context, the UNSO underpins subsidiary regulations such as the JCPOA-Iran Regulation and the DPRK Regulation, which impose restrictions on arms transfers, nuclear and ballistic missile-related items, and the financial assets of designated persons. Estate agents must comply with these sanctions as a statutory obligation and ensure that no property transaction under their facilitation benefits designated persons.

- The United Nations Sanctions (Joint Comprehensive Plan of Action – Iran) Regulation (Cap. 537BV) (the “JCPOA – Iran Regulation”) implements UNSC Resolution 2231 by prohibiting the transfer of conventional arms, nuclear-related items, and ballistic missile-related items to or from Iran, and restricting the economic assets of designated persons. Estate agents must not facilitate property transactions benefiting designated persons.

- The United Nations Sanctions (Democratic People’s Republic of Korea) Regulation (Cap. 537AE) (the “DPRK Regulation”) implements UNSC sanctions on the DPRK by prohibiting arms supply, restricting proliferation-related financial transactions, and freezing economic assets of designated persons and entities. Estate agents must screen clients against the sanctions list and ensure no transaction deposits reach designated persons or entities.

Other Legislation

- The Cross-boundary Movement of Physical Currency and Bearer Negotiable Instruments Ordinance (Cap. 629) (the “Ordinance”) establishes a declaration and disclosure system to detect the cross-boundary transportation of large quantities of currency and bearer negotiable instruments (CBNIs) into and out of Hong Kong for AML/CFT purposes. Estate agents should be aware that persons carrying CBNIs with a total value exceeding HK$120,000 (or the equivalent in foreign currencies) are required to declare them to Customs, and any failure to declare or false declaration may indicate ML/TF activity warranting a suspicious transaction report.

- In addition, the Estate Agents Ordinance provides a regulatory framework for estate agents, covering licensing, conduct, and compliance expectations in the real estate sector. It complements AML/CFT obligations by empowering the EAA to supervise the sector and take disciplinary action for non-compliance.

Strengthen AML Compliance for Estate Agents in Hong Kong

Identify and manage ML/TF risks in your estate agency business.

Regulatory Guidelines Applicable to Estate Agents in Hong Kong

- Estate agents in Hong Kong must follow detailed AML/CFT guidelines issued by the Estate Agents Authority (EAA), which outline expectations for AML/CFT compliance in the estate agency sector. These guidelines expand on statutory obligations and provide practical implementation steps. The current AML/CFT circular is Practice Circular No. 23-01(CR), which includes a five-year record retention requirement for CDD and transaction records.

- The estate agent AML guidance requires firms to verify beneficial ownership, identify buyers, and understand the purpose of transactions. Enhanced due diligence is necessary for high-risk scenarios such as high-value cash property deals, complex structures or PEP identification.

- Ongoing monitoring is also essential under the AML framework. Estate agents must monitor transactions to detect unusual patterns, including the use of third-party purchasers or rapid resale of luxury property.

- The EAA expects estate agents to maintain vigilance throughout the transaction lifecycle, rather than solely relying on initial checks.

In practice, estate agents should be able to show customer identification records, beneficial ownership checks, risk assessment notes, sanctions and PEP screening results, internal escalation records, STR decision records, staff training records, and copies of policies and procedures. This helps demonstrate that AML/CFT controls are not merely documented but actually implemented.

AML/CFT Regulatory Authorities for Estate Agents in Hong Kong

The Estate Agents Authority (EAA) is the primary supervisory body responsible for overseeing AML/CFT-related regulations among estate agents. It issues AML/CFT guidelines and circulars for estate agents in Hong Kong and monitors adherence to statutory obligations within the real estate sector.

Under EAO, the estate agents’ authority is responsible for granting and overseeing licenses to estate agents. Further, estate agents and salespersons must pass the fit-and-proper test.

EAA expects estate agents to demonstrate effective implementation of CDD requirements. It further requires maintaining adequate documentation and responding promptly to regulatory inquiries.

Through supervision and enforcement, these authorities strengthen the integrity of the real estate sector.

Navigate AML Regulations with Confidence

We help you meet estate agents’ AML CDD requirements and the regulatory expectations in Hong Kong

AML/CFT Law Enforcement Agencies for the Estate Agents Sector

Law Enforcement Agencies (LEAs) play a critical role in investigating and prosecuting money laundering cases involving estate agents. These agencies support the enforcement of Hong Kong’s AML/CFT framework by working closely with regulators to identify suspicious activities.

- Hong Kong Police Force (HKPF)

- Customs and Excise Department (C&ED)

- Independent Commission Against Corruption (ICAC)

Joint Financial Intelligence Unit (JFIU) in Hong Kong

- The Joint Financial Intelligence Unit (JFIU) is a joint unit operated by the Hong Kong Police Force (HKPF) and the Customs and Excise Department (C&ED).

- The JFIU receives and analyses Suspicious Transaction Reports (STRs) filed by estate agents in Hong Kong and disseminates financial intelligence to relevant law enforcement agencies for investigation and enforcement.

- The JFIU also identifies common Money Laundering/Terrorist Financing (ML/TF) typologies and emerging risks relating to the real estate sector and contributes to the territory’s AML/CFT intelligence framework.

Hong Kong NRA, SRA, and Risks Associated with Estate Agents

The Estate Agents Sector in Hong Kong is rated as Medium-Low Risk because of the following ML Threats and Vulnerabilities:

ML Threats in the Real Estate Sector (medium-low)

- Estate agents are not typically part of the whole fund-flow chain as they act only as middlemen, facilitating only the initial deposits, making them less vulnerable to ML threats. However, high-value transactions may expose the real estate sector to ML risks.

ML Vulnerabilities in the Real Estate Sector (medium-low)

- Estate agents in Hong Kong are likely less vulnerable to emerging ML risks compared to solicitors or banks, with a risk rating of medium-low.

- As middlemen, they handle only a small portion of the total price, typically 3-5% (rarely cash).

- Also, estate agents are required to follow strict AMLO requirements, licensing requirements, including fit-and-proper tests, with strict supervision by the Estate Agents Authority, making the sector less vulnerable to ML risks.

Mitigate AML Risks in Property Transactions

Train your compliance team to assess risks in your real estate business to identify high-risk clients, avoid penalties and prevent financial crime.

FATF and APG Guidelines Concerning Estate Agents

- The Financial Action Task Force (FATF) and the Asia/Pacific Group on Money Laundering (APG) provide international standards that influence Hong Kong’s AML framework. These organisations emphasise the importance of regulating DNFBPs, including estate agents.

- Their guidance highlights the risks associated with the real estate sector, particularly in transactions involving property buyers and cross-border investments. The estate agents’ AML Guidelines reflect these global standards.

- FATF recommendations stress the importance of Customer Due Diligence (CDD), beneficial ownership transparency, and Suspicious Transaction Reporting (STR). These regulations are embedded in Hong Kong’s regulatory approach.

- Alignment with FATF and APG ensures Hong Kong’s estate agency AML regime meets international standards.

How AML Consultants HK Helps Estate Agents in Hong Kong Implement AML Laws

AML Consultants HK provides comprehensive support to estate agents operating in Hong Kong’s real estate sector, ensuring alignment with estate agents’ AML guidelines and regulatory expectations.

They offer an AML Compliance Advisory to help firms interpret and implement CDD requirements effectively. Through an AML Independent Audit, they assess the effectiveness of existing controls and identify gaps.

ML/TF Risk Assessments service enables estate agents to evaluate the exposures to risks such as high-value cash property deals and offshore property transactions, and develop control measures. AML/CFT Training equips staff with the knowledge required to manage compliance obligations.

Additionally, AML Regulatory Reporting ensures that estate agents remain updated on evolving AML regulations, helping them maintain continuous compliance.

2) Understand how regulated entities are classified, the AML/CFT legal framework in Hong Kong, and the compliance requirements that apply to each group:

FAQs on AML Laws for Estate Agents in Hong Kong

Should estate agents charge for AML checks?

Estate agents may recover compliance-related costs depending on their commercial terms, but AML checks themselves are a compliance obligation and should not be treated as optional.

What AML/CFT laws govern estate agents in Hong Kong?

Key laws include AMLO, OSCO, UNSO, UNATMO, EAO, and DTROP. They establish CDD, record-keeping requirements and reporting obligations.

Why are estate agents vulnerable to money laundering risks?

The real estate sector involves high-value transactions and complex ownership structures, which makes it attractive for laundering illicit funds.

What is the role of the Estate Agents Authority (EAA) in AML/CFT?

EAA issues guidelines, monitors compliance, and conducts inspections. It ensures estate agents follow AML regulations.

How do Hong Kong regulators monitor real estate businesses?

They conduct audits, inspections, and review compliance records. Monitoring ensures adherence to AML/CFT compliance requirements.

About the Author

Pathik Shah

Founder | FCA, CAMS, CISA, CS, DISA (ICIAI), FAFP (ICAI)

Pathik Shah is a Chartered Accountant with more than 28 years of experience working at the juncture of governance, compliance, and financial risk. His work has consistently focused on helping institutions in Hong Kong to operate confidently within regulated environments, particularly where AML/CFT obligations demand practical implementation.

As part of his role with AML Consultants HK, Pathik is involved in working with various financial institutions and DNFBPs so that not only are their AML frameworks compliant from a regulatory standpoint under the Anti-Money Laundering and Counter-Terrorist Financing Ordinance (Cap. 615), but they are also effective from a supervisory review expectations standpoint. Aside from that, Pathik has served as a functional expert in the development and deployment of RegTech solutions to enhance monitoring discipline and documentation integrity. Additionally, he has assisted institutions in understanding the FATF requirements and how to implement them within the Hong Kong context in an operationally feasible manner.

Pathik is a recognised thought leader in AML/CFT and frequently shares insights on trends in financial crime risks and developing supervisory approaches on various platforms.