Table of Contents

- March 19, 2026

- Pathik Shah

AML/CFT Legal Framework for Banks in Hong Kong- Key Takeaways

- The core AML/CFT legal framework for banks in Hong Kong includes AMLO, DTROP, OSCO, UNATMO, WMDO, UNSO, and BO.

- The AML/CFT regulatory authority for banks is the Hong Kong Monetary Authority (HKMA).

- The LEAs and FIUs in the banking sector include HKPF, C&ED, ICAC, and JFIU.

- AML Consultants HK helps in implementing the legal framework for Banks in Hong Kong by conducting EWRA, setting up in-house compliance, and designing AML/CFT systems.

Scope and Applicability

The AML/CFT legal framework for banks in Hong Kong includes key laws, regulatory guidance, and supervisory authorities.

The framework is applicable to Authorized Institutions (AIs), which include licensed banks, restricted licence banks, and deposit-taking companies regulated by HKMA and required to stay compliant with AML regulations under AMLO compliance to prevent ML/TF/PF risks.

Banks are also required to implement a risk-based approach, CDD, EDD, maintain records, and submit STR to JFIU via STREAMS 2 as a part of their bank AML obligations. Non-compliance with certain regulations can result in penalties, imprisonment, or public reprimands.

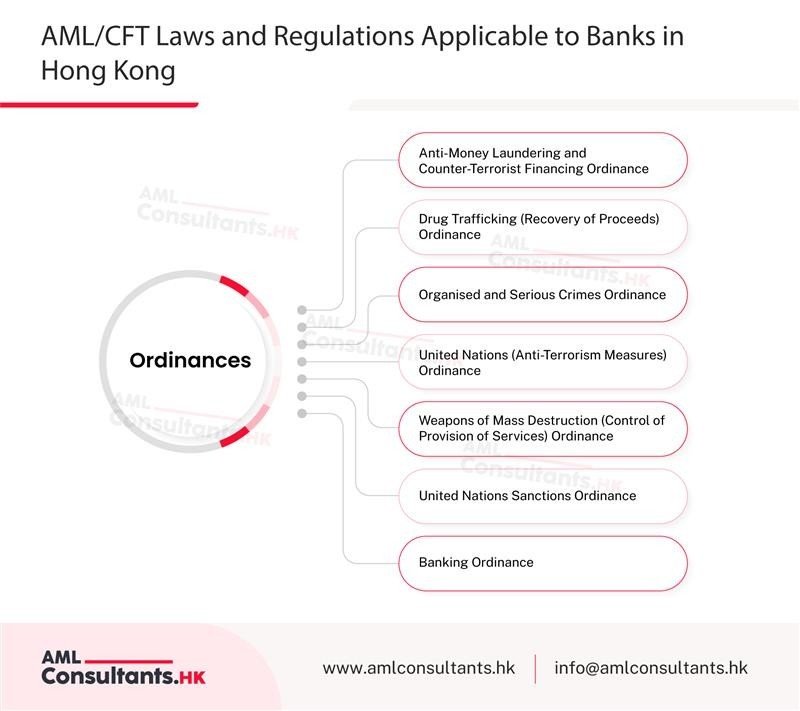

AML/CFT Laws and Regulations Applicable to Banks in Hong Kong

The main legislation relevant for banks is the AMLO, which obligates them to CDD and record-keeping requirements, and the Banking Ordinance, which requires AIs to maintain an adequate system of controls.

The AML/CFT legal framework for banks in Hong Kong is as follows:

Anti-Money Laundering and Counter-Terrorist Financing Ordinance (AMLO)

AMLO is the primary statutory framework which banks must follow to prevent financial crime. The AMLO framework, read together with the HKMA AML/CFT Guideline, sets out requirements relating to CDD, ongoing monitoring, correspondent banking controls, and senior management approval for higher-risk correspondent banking relationships.

Drug Trafficking (Recovery of Proceeds) Ordinance

DTROP is the law in Hong Kong for banks, which is designed to trace, confiscate, and recover proceeds from crime linked with drug trafficking, it makes it offence for banks and their employees to dealing with such proceeds, they required them to file STR as or such crimes, DTROP also criminalise dealing with property that represent drug proceeds and requires banks to avoid tipping off.

Organised and Serious Crimes Ordinance (OSCO)

OSCO is the key law in Hong Kong for banks, and it aims to target money laundering arising from organised and serious crimes and allows asset restraint and confiscation linked to proceeds of crime. It creates an obligation for banks and makes it a criminal offence for them to deal with property linked with such proceeds, and requires banks to avoid tipping off. Non-compliance will lead to penalties.

United Nations (Anti-Terrorism Measures) Ordinance (UNATMO)

UNATMO was made to follow the United Nations rules to prevent and stop terrorism. The law prohibits banks from providing support in the form of money or property and allows authorities to freeze such assets.

Weapons of Mass Destruction (Control of Provision of Services) Ordinance (WMDO)

WMDO is the AML/CFT Legal Framework for Banks in Hong Kong that restricts the services that may assist the development, production, or acquisition of weapons capable of causing mass destruction. The law prohibits banks from providing any specific services, including lending money. Banks may face serious penalties for non-compliance, including unlimited fines and imprisonment for up to seven years.

United Nations Sanctions Ordinance (UNSO)

UNSO is the law that prohibits banks from providing services or conducting transactions linked with sanctioned parties and requires them to strictly adhere to rules and regulations.

Banking Ordinance

The Banking Ordinance supervises deposit-taking companies and banks in Hong Kong. The law helps in ensuring stability and integrity in the banking system in Hong Kong, builds public confidence in the financial system, and protects depositors.

Need Help Implementing the AML/CFT Legal Framework for Banks in Hong Kong?

AML Consultants HK ensures your compliance framework aligns with AML regulations, supervisory expectations, and FATF standards.

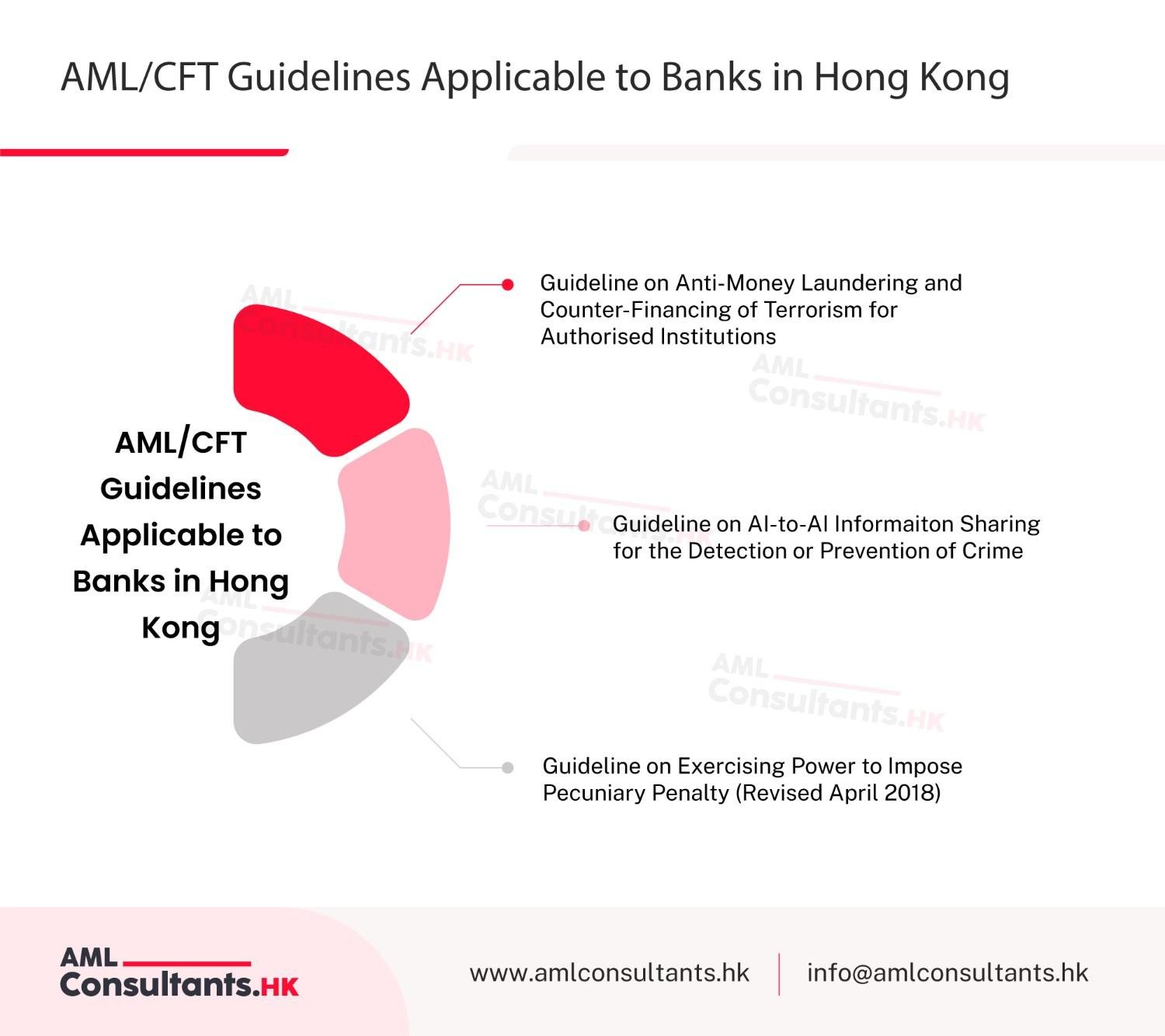

AML/CFT Guidelines Applicable to Banks in Hong Kong

AML/CFT guidelines issued by the Monetary Authority (MA) set out the AML/CFT statutory and regulatory requirements. They set out the AML/CFT standards that AIs must comply with, the manner in which the HKMA proposes to exercise its power to impose a pecuniary penalty, and guidance for AIs on the information-sharing mechanism.

1. Guideline on Anti-Money Laundering and Counter-Financing of Terrorism for Authorized Institutions

The principal AML/CFT statutory guideline applicable to banks in Hong Kong is the Guideline on Anti-Money Laundering and Counter-Financing of Terrorism (For Authorized Institutions) (Revised May 2023), issued by the HKMA under section 7 of AMLO and section 7(3) of the Banking Ordinance.

The core principle of this guideline is to implement a risk-based approach to identify, assess, and understand specific risks and implement measures to mitigate those risks. It also requires implementation of AML/CFT systems, implementing the CDD measures, monitoring transactions such as wire transfers and cross-border fund movement, staff training, and record-keeping, typically for at least 5 years.

Failure to comply with AML/CFT statutory or regulatory requirements may lead to supervisory or disciplinary action by the HKMA, which can include pecuniary penalties, remedial directions, and public reprimand, depending on the facts and severity of the case.

2. Guideline on AI-to-AI Information Sharing for the Detection or Prevention of Crime

The Guideline on AI-to-AI Information Sharing for the Detection or Prevention of Crime was published by the HKMA in November 2025. It describes the statutory framework and regulatory expectations for the voluntary sharing of information among authorized institutions for the purpose of detecting or preventing prohibited conduct (the information-sharing mechanism).

3. Guideline on Exercising Power to Impose Pecuniary Penalty (Revised April 2018)

The HKMA has issued a guideline under Section 23(1) of the Anti-Money Laundering and Counter-Terrorist Financing Ordinance (Chapter 615), which provides guidance on factors to be considered by the MA when imposing a pecuniary penalty.

AML/CFT Regulatory Authorities for Banks in Hong Kong

The AML/CFT regulatory authority for banks is the Hong Kong Monetary Authority (HKMA), which serves as a central banking institution for Hong Kong.

HKMA was established on 1st April 1993 and supervises authorized institutions’ (AIs) risk management systems for combating ML/TF risks.

It also implements a banking regulatory and supervisory regime, including policies, legislation, and standards. The HKMA also manages the exchange fund’s reserves. It also ensures compliance by providing various regulatory resources.

Is your AML Framework Truly Compliant?

AML Consultants HK helps in identifying gaps, strengthening controls, and ensuring your AML Program meets regulatory expectations.

AML/CFT Law Enforcement Agencies in the Banking Sector

AML/CFT law enforcement agencies under the AML/CFT legal framework for banks in Hong Kong include:

Hong Kong AML/CFT Law Enforcement Agencies in the Banking Sector

- Hong Kong Police Force (HKPF)

- Customs and Excise Department (C&ED)

- Independent Commission Against Corruption (ICAC)

FIU Hong Kong

Hong Kong Joint Financial Intelligence Unit (JFIU) is jointly run by HKPF and C&ED, and it is the sole agency managing the suspicious transaction reporting regime.

Hong Kong NRA, SRA, and Risks Associated with Banks

Hong Kong conducts national risk assessment and sectoral risk assessment to identify threats and vulnerabilities to money laundering and terrorist financing. Under Hong Kong’s 2022 NRA/HRA, the banking sector’s money laundering risk is assessed as high, with high threat and medium-high vulnerability. The banking sector is often considered high-risk due to its threats and vulnerabilities, including:

Threats

- Online fraud, including cross-border fund movement.

- Corruption and tax crimes are a significant source of illicit proceeds.

- Misuse of international wire transfers to move illicit proceeds across jurisdictions, facilitating rapid fund flow across various accounts.

- Some of the other threats also include proceeds generated from crimes such as drug trafficking, gambling, and smuggling, often laundered using shell companies.

Vulnerabilities

- Remote customer onboarding through non-face-to-face channels increases vulnerabilities to impersonation fraud and account takeover risk.

- Using mule account networks to launder illicit proceeds.

- Using new payment methods, such as faster payment systems, which offer speed and anonymity that can be exploited to move illicit funds easily.

Build A Smarter AML Defence for Your Bank

Identify ML/TF/PF risks and implement effective AML policies with expert guidance.

FATF and APG Guidelines Concerning Banks

The Financial Action Task Force (FATF) and Asia/Pacific Group on Money Laundering (APG) work together to set and enforce global standards for financial crime. Hong Kong has been actively participating with FATF since 1991 and with APG since 1997.

The FATF sets the forty FATF recommendations, which say that countries must follow rules to prevent ML/TF risks. It also essentially required the private sector, including banks, to detect and stop the misuse of the financial system. Banks are also expected to use a risk-based approach when dealing with high-risk clients and should also monitor the FATF’s black and grey lists to apply extra checks on transactions involving risky countries.

The APG examines ML/TF typologies and recent trends, helping banks to develop policies and strategies to combat financial crime. The APG basically helps in ensuring that the rules are accurately applied across the Asia-Pacific region and helps the banks to stay compliant with AML/CFT regulations.

How AML Consultants HK Help in Implementing Legal Framework for Banks in Hong Kong

AML Consultants HK helps in implementing the legal framework for banks in Hong Kong by conducting an enterprise-wide risk assessment (EWRA), which helps in identifying the company’s risks and evaluating control effectiveness.

AML Consultants helps in setting up in-house compliance, which enables banks to strengthen internal controls and establish clear reporting lines.

AML Consultants HK also helps banks in designing an AML/CFT system, which includes policies and procedures, helping in counter ML/TF/PF risks.

FAQs-AML/CFT Legal Framework for Banks in Hong Kong

What is the main AML law governing banks in Hong Kong?

The main AML/CFT legal framework for banks in Hong Kong is the Anti-Money Laundering and Counter-Terrorist Financing Ordinance (AMLO).

What are the customer due diligence requirements for banks under Hong Kong AML regulations?

The CDD requirements for the banks under Hong Kong AML regulations require them to verify and identify the customer, conduct continuous monitoring, and retain records for at least 5 years.

When must banks in Hong Kong perform enhanced due diligence on customers?

The banks in Hong Kong must perform EDD on customers in high-risk scenarios, such as when the customer is a PEP or when dealing with correspondent banking.

How does the Hong Kong Monetary Authority supervise AML compliance in banks?

The HKMA supervises AML compliance in banks through key methods, including risk management systems, issuing guidelines, and ongoing assessment and investigations.

About the Author

Pathik Shah

Founder | FCA, CAMS, CISA, CS, DISA (ICIAI), FAFP (ICAI)

Pathik Shah is a Chartered Accountant with more than 28 years of experience working at the juncture of governance, compliance, and financial risk. His work has consistently focused on helping institutions in Hong Kong to operate confidently within regulated environments, particularly where AML/CFT obligations demand practical implementation.

As part of his role with AML Consultants HK, Pathik is involved in working with various financial institutions and DNFBPs so that not only are their AML frameworks compliant from a regulatory standpoint under the Anti-Money Laundering and Counter-Terrorist Financing Ordinance (Cap. 615), but they are also effective from a supervisory review expectations standpoint. Aside from that, Pathik has served as a functional expert in the development and deployment of RegTech solutions to enhance monitoring discipline and documentation integrity. Additionally, he has assisted institutions in understanding the FATF requirements and how to implement them within the Hong Kong context in an operationally feasible manner.

Pathik is a recognised thought leader in AML/CFT and frequently shares insights on trends in financial crime risks and developing supervisory approaches on various platforms.